The Internet of Things (IoT) era has spawned many technological innovations. Gartner estimates that there will be over 20 billion devices by 2020, with spending on IoT related services to reach up to $3 trillion. One such service touted to be the next big disruption in the banking industry is the Internet of Payments (IoP).

Internet of Payment enables payment processing over IoT devices such as automobiles, appliances, and wearables.

Visa and Mastercard are pioneering IoP services by introducing solutions for financial institutions aimed at provisioning seamless card payments over connected devices. With the proliferation of Open Banking, even Fintechs and third-party providers can act as IoP service providers giving banks more flexibility to collaborate and innovate. We are also seeing increasing collaboration between major payment networks and IoT device manufactures to launch payment platforms for the consumers.

Popular examples are Fitbit enabling payments with the wave of a hand, GM Cars and Honda Cars having an in-car app to enable seamless payments, shopping groceries using Samsung refrigerators, and payments using smart home assistants such as Amazon Alexa, Google Home.

Consumers expect speed of transaction and ease of use more than before as payments are now made convenient from any device anytime without friction. To supersede this preferred method, IoP services need to deliver extraordinary convenience. Securing payments is one such service IoP can offer. General Data Protection Regulation (GDPR), Federal Trade Commission (FTC), Payment Card Industry Data Security Standard (PCI DSS) and other regulations are some of the norms institutions need to comply with in regard to securing Personally Identifiable Information (PII).

Tokenization can be a fool proof industry standard acceptable by major payment networks to help keep transactions private and secure. Additionally, with card-on-file EMV tokenization, merchants only store tokens in their database instead of card details. EMV Co. published the initial version of the Tokenization framework in March 2014, that will enable a new generation of payment products and at the same time, help leverage existing payments infrastructure.

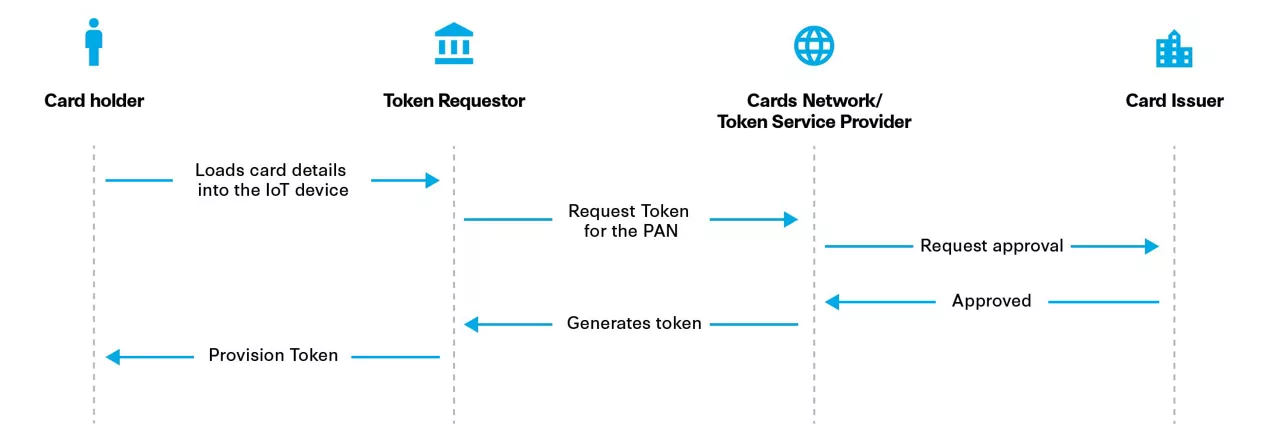

How are card details tokenized in the IoP ecosystem?

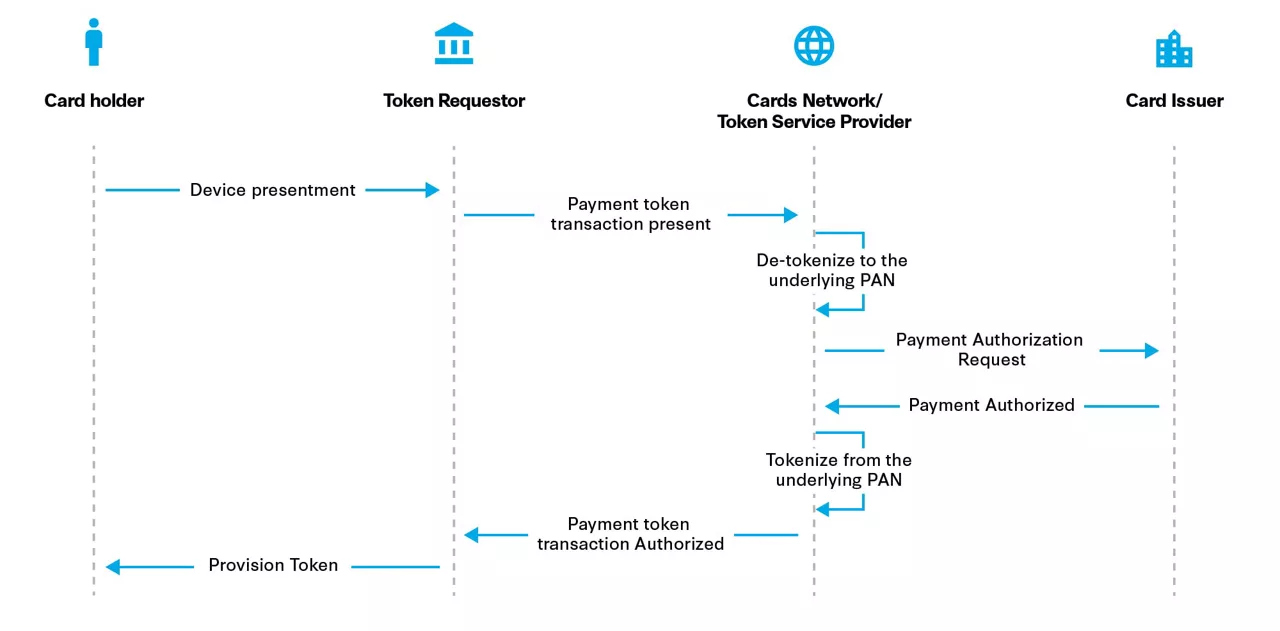

How are tokenized payments authorized?

Although at a nascent stage, regulatory bodies, recognizing the growing trend of payments through IoT devices, are framing compliance laws to regulate IoP.

Internet of Payments enables better customer-connect, together with the larger IoT ecosystem. It also contributes to increased revenues by virtue of additional volume and opening new ways of fulfilling payments. And herein lies an opportunity for Fintechs and Big techs to gain a foothold in the banking and financial industry, by introducing new business models.

Traditional players, hitherto going strong in the banking and financial industry need to quickly adapt to the opportunities and subsequent disruption that IoP will bring to stay competitive, while retaining existing customers and attracting new ones.

The future looks even more promising with payments through injectables and implantations. Financial institutions should invest and continue to do so in researching new trends and build the infrastructure to take advantage of IoP to stay ahead in this digital world and deliver delightful customer experiences.

Subscribe to keep up-to-date with recent industry developments including industry insights and innovative solution capabilities